Buying guide

Home loan cash back: a guide for home buyers & refinancers

Beware the free money

AI summary

Home loan cashback is a cash payment, typically 0.6% to 1% of your loan, offered by banks to attract new customers or those refinancing from another lender.

This incentive comes with a crucial condition: a "clawback period" of 3-4 years. If you sell, repay your loan, or refinance within this timeframe, you must repay a portion of the cashback.

To compare offers, calculate your total loan cost over the clawback period and subtract the cashback amount.

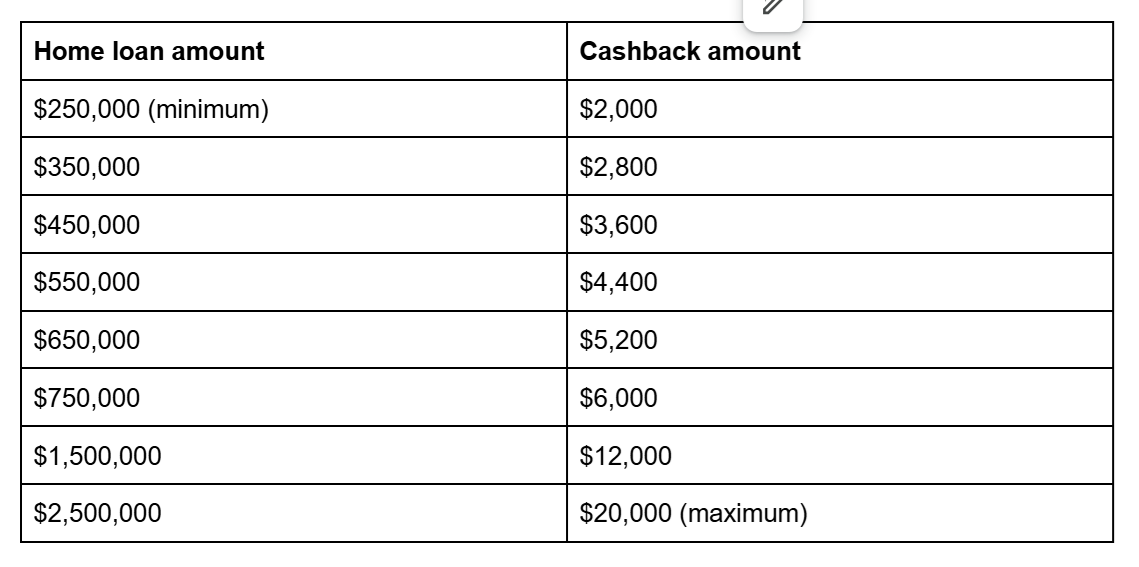

How much is home loan cashback?

Examples of cash back amounts (0.8% cashback)

(This is just an example - actualy cashback ammounts may vary)

What can I do with the cash?

Who’s eligible for a home loan cash contribution?

Cashback can make a big difference.

Beware the claw back period

How to compare loans with mortgage cashbacks

Can I get a mortgage cashback if I already have a mortgage?

Have you refinanced to get cashback lately?

Are mortgage cashbacks worth it?

Author

Discover More

Built for the nation – The classic Kiwi state house (1930s–1950s)

Built with native timbers, classic Kiwi state houses combine mid-century durability with the ultimate renovation canvas.

The 8 Best Landscaping Companies in Wellington (According to Online Reviews)

Can’t beat a Wellington garden on a good day

Search

Other articles you might like