Buying guide

How does Kiwisaver first home withdrawal work?

There are a few things you need to know if you want to withdraw your Kiwisaver to buy a home

AI summary

Using your KiwiSaver first home withdrawal can help you buy property. To be eligible, you must have contributed for at least three years and intend to live in the home for at least six months.

Apply directly through your KiwiSaver provider, not Kāinga Ora. It's crucial to apply early with a signed sale and purchase agreement, as funds must be ready before the sale goes unconditional. Delays can risk the purchase. Consider moving to a conservative fund to protect your deposit.

Kiwisaver first home withdrawal rules for eligibility

The process: Using Kiwisaver for your first home

Applying for pre-approval or confirming the amount you can withdraw

To apply for a Kiwisaver withdrawal contact your fund provider.

Applying to for Kiwisaver withdrawal: First home buyers

Stuff you need to know when using Kiwisaver for your first home

You can put your first home Kiwisaver withdrawal towards your purchase deposit

It’s important to ensure your Kiwisaver funds are ready in time

You’ll need to intend live in the home for at least six months

-fotor-20240408171748.jpg)

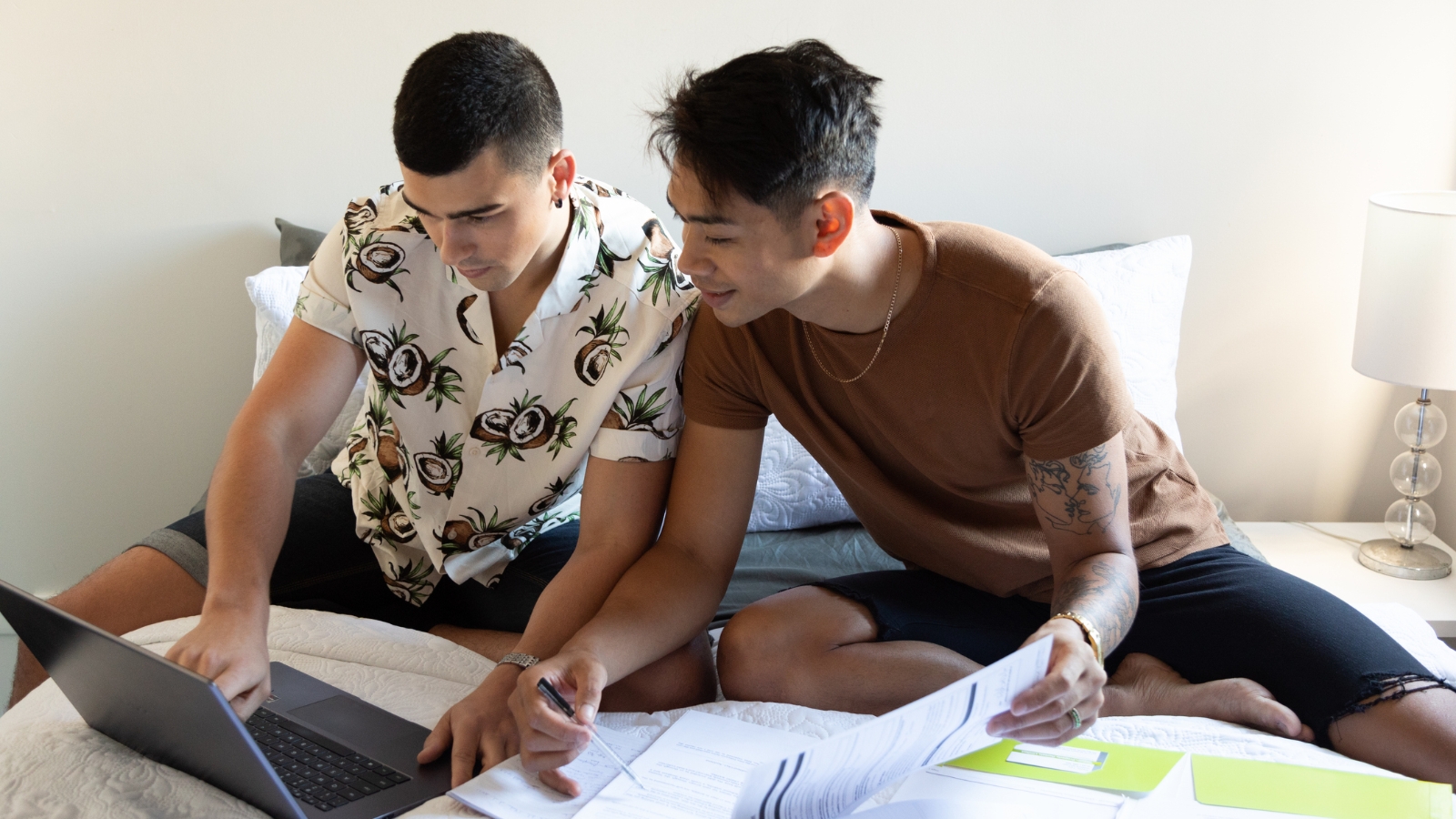

Withdrawing from your Kiwisaver can be a great way to secure your first home.

Be smart with your Kiwisaver before purchasing a home

Author

Discover More

The five places where first-home buyers are winning the most

The five regions where first-home buyers are buying the biggest share of homes in New Zealand.

From an empty paddock at the end of a gravel road, they built an off-grid haven – complete with a Love Bus

A bare paddock became an award-winning off-grid escape with tiny homes, a Love Bus and coastal views.