Buying guide

NZ Construction loans: Everything you need to know (2025)

The Trade Me Property guide to financing your next build

AI summary

Building a home? A construction loan is key. You'll typically need a deposit of at least 10% of the total land and build cost.

Unlike a standard mortgage, funds are drawn down in stages to pay your builder as work progresses. You may have interest-only payment options during the build. To apply, you'll need a builder's contract, consents, and a valuation. Consider if a simple Turn key package or a more flexible Build-only contract suits you best.

How much deposit do I need for a construction loan?

How do construction loans work?

How to apply for a construction loan

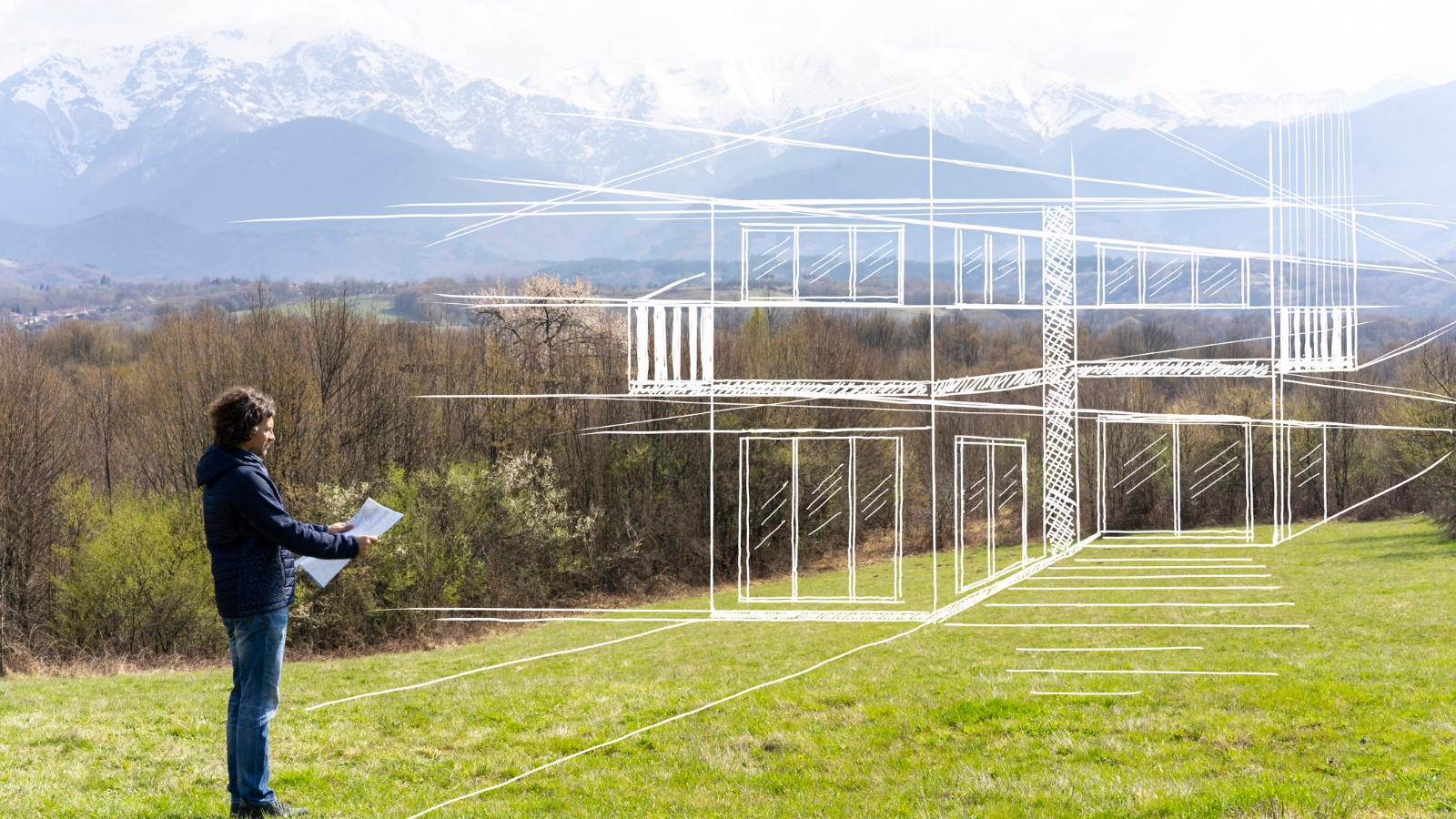

You won't get far without finance.

How much can I borrow with a construction loan?

A closer look at construction loan progress payments

Types of construction contracts

1. Turn key

2. Build-only

-fotor-2024080816437.jpg)

The right loan can make building much easier.

A note on provisional costs (PCs)

Finding the right construction loan

Author

Discover More

From an empty paddock at the end of a gravel road, they built an off-grid haven – complete with a Love Bus

A bare paddock became an award-winning off-grid escape with tiny homes, a Love Bus and coastal views.

The five places where first-home buyers are winning the most

The five regions where first-home buyers are buying the biggest share of homes in New Zealand.

Search

Other articles you might like