Buying guide

Fixed, floating or split mortgage?

Understand your options

6 December 2023

AI summary

Choosing the right mortgage structure is crucial. A fixed rate mortgage provides payment certainty for a set term but limits extra repayments and can have break fees. In contrast, a floating rate loan offers flexibility for lump sum payments, but your repayments can rise unexpectedly.

A popular strategy is a split mortgage, which combines both types to balance security with flexibility. This allows you to tailor your loan structure to your financial goals. Seeking personalised advice from a mortgage adviser is highly recommended.

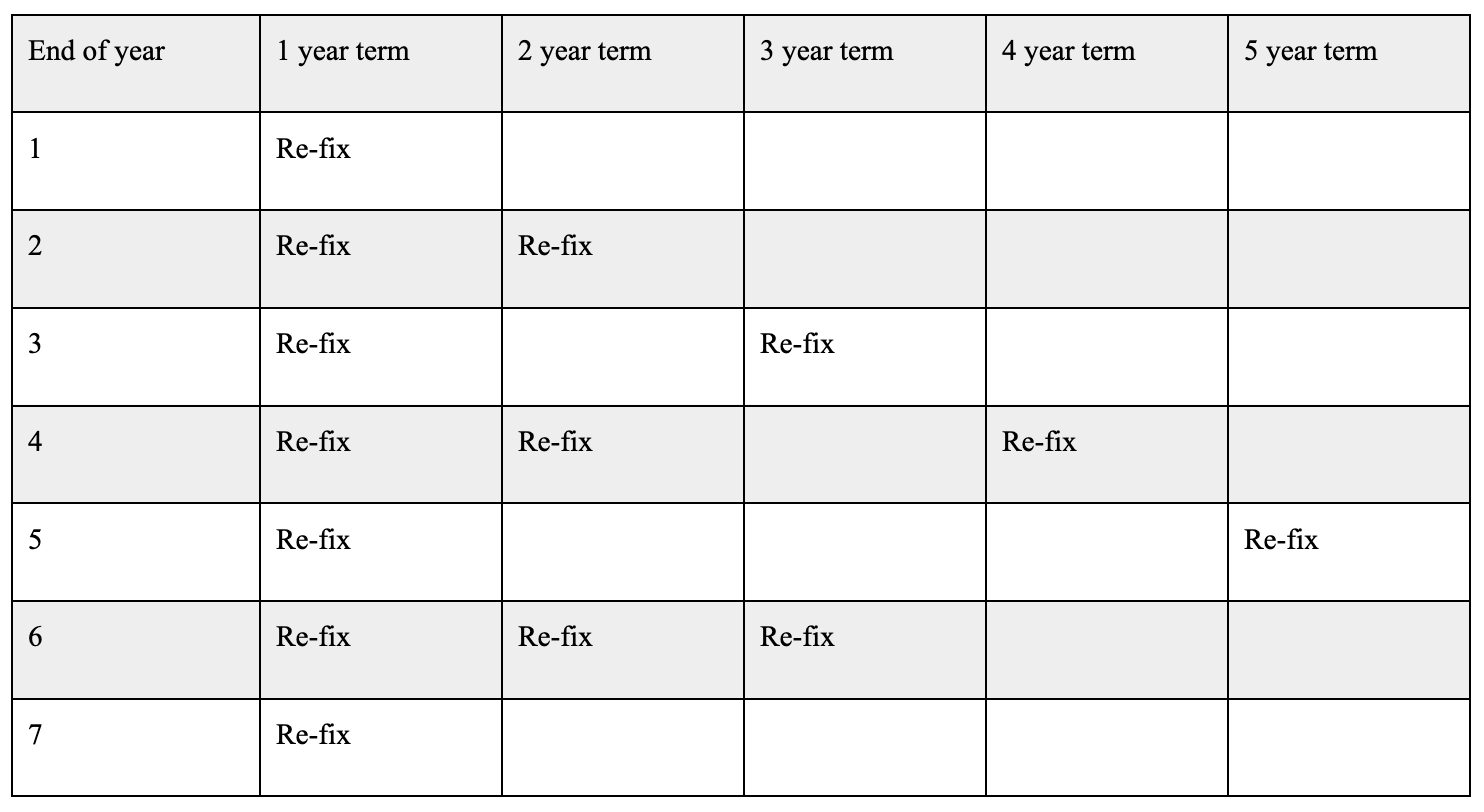

How does a fixed mortgage work?

Choosing a fixed rate term

There may be some repayment flexibility with a fixed mortgage

How does a floating mortgage work?

Why do floating rates change?

What are the different types of mortgages?

Examples of possible mortgage structures

Getting experienced advice

Authors

Discover More

The five places where first-home buyers are winning the most

The five regions where first-home buyers are buying the biggest share of homes in New Zealand.

From an empty paddock at the end of a gravel road, they built an off-grid haven – complete with a Love Bus

A bare paddock became an award-winning off-grid escape with tiny homes, a Love Bus and coastal views.

Search

Other articles you might like