Discover

Understanding the meaning of mortgage acronyms and terminology

Here’s a quick explanation of what the main mortgage terms mean to help you start talking like a pro.

AI summary

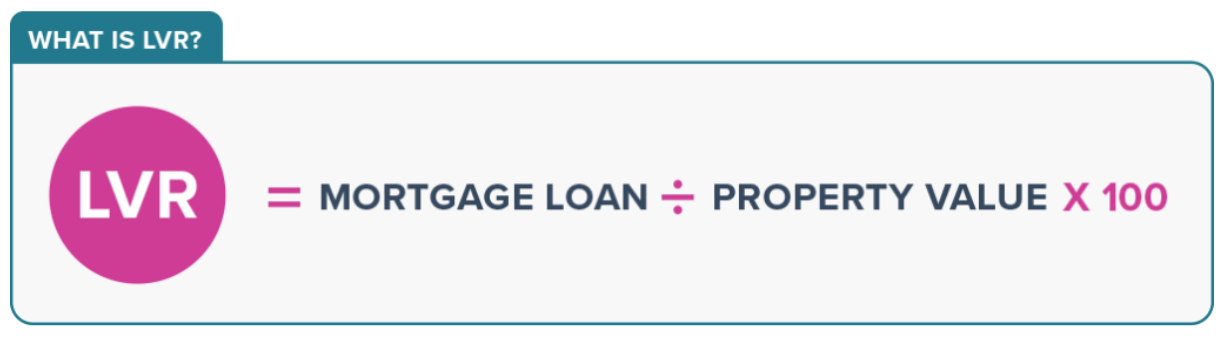

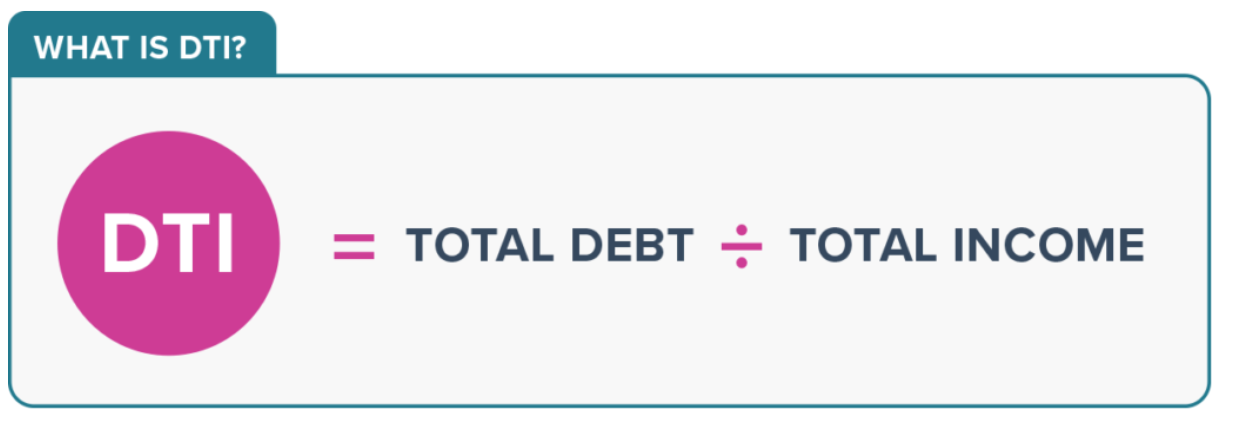

Understanding mortgage jargon is crucial for Kiwi home buyers. Key terms include LVR (Loan-to-Value Ratio), which compares your loan to the property's value, and DTI (Debt-to-Income Ratio), which measures your total debt against your income. The Reserve Bank is considering DTI limits.

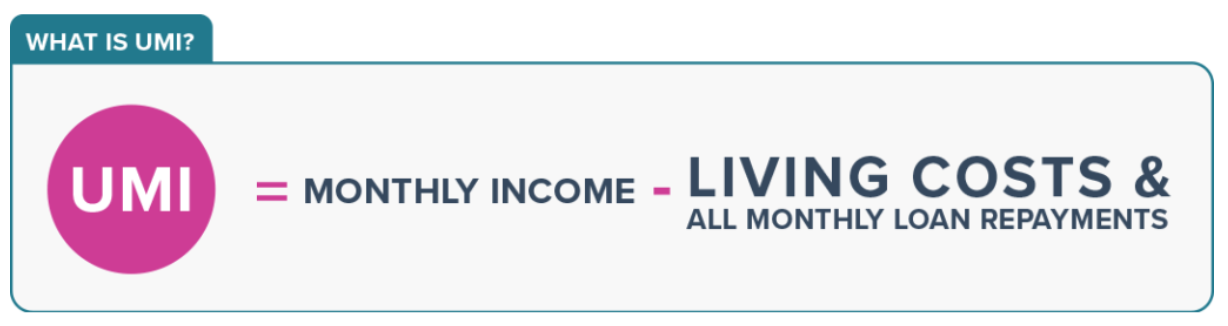

Other important concepts are UMI (Uncommitted Monthly Income), your monthly surplus after expenses, and AML (Anti-Money Laundering) laws requiring identity verification. Your credit score reflects your ability to manage debt and influences loan approval.

What does LVR mean?

Image provided by mortgages.co.nz

What does DTI mean?

Image provided by mortgages.co.nz

What does UMI mean?

Image provided by mortgages.co.nz

What does AML mean?

What is a credit score?

Authors

Discover More

The five places where first-home buyers are winning the most

The five regions where first-home buyers are buying the biggest share of homes in New Zealand.

From an empty paddock at the end of a gravel road, they built an off-grid haven – complete with a Love Bus

A bare paddock became an award-winning off-grid escape with tiny homes, a Love Bus and coastal views.

Search

Other articles you might like