News Next article

Aotearoa rental market flatlines as national rent stalls

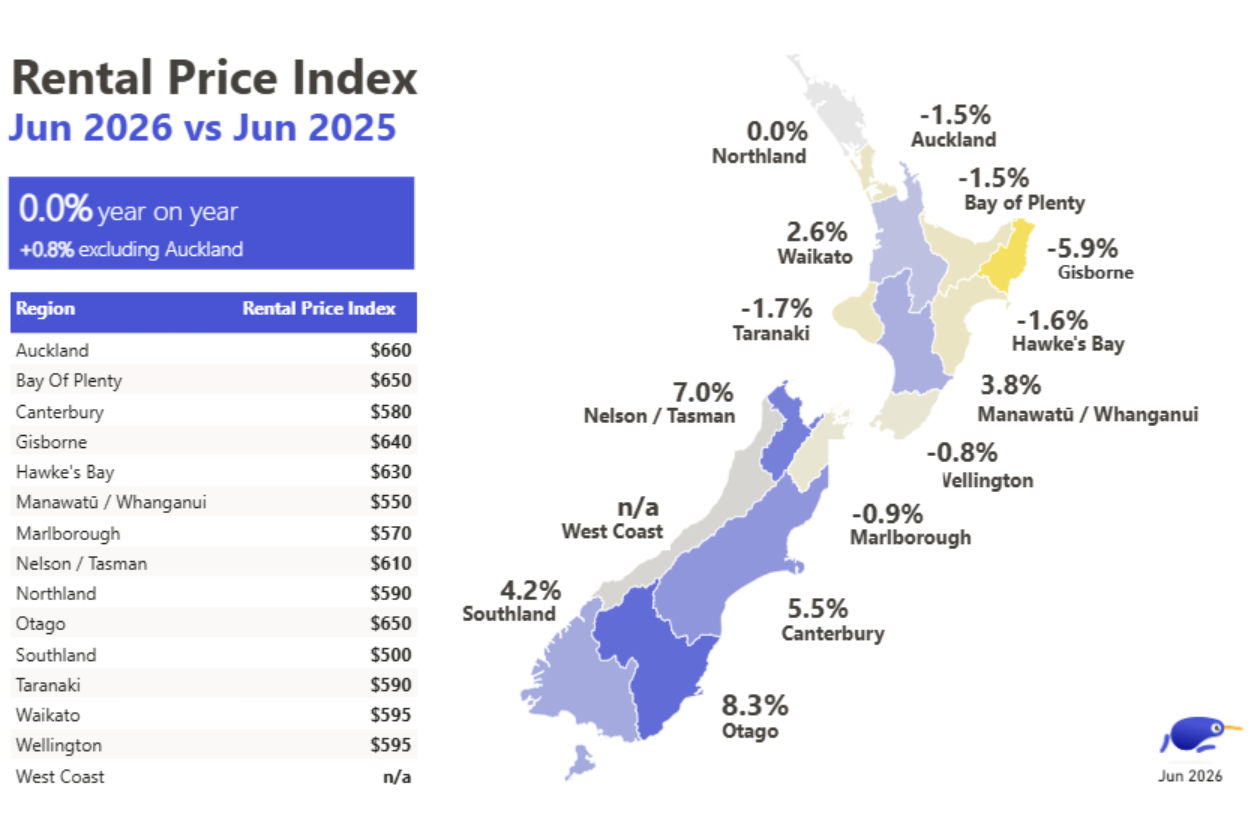

Rental Price Index - June 2026

By Casey Wylde 22 July 2026

Median weekly rents by region, June 2026

Southern regions heat up while main centers cool

Demand remains strong despite seasonal dip

| Region | Rental Price Index | ||

|---|---|---|---|

| Auckland | Auckland | $660 | $660 |

| Bay of Plenty | Bay of Plenty | $650 | $650 |

| Canterbury | Canterbury | $580 | $580 |

| Gisborne | Gisborne | $640 | $640 |

| Hawke's Bay | Hawke's Bay | $630 | $630 |

| Manawatu/Whanganui | Manawatu/Whanganui | $550 | $550 |

| Marlborough | Marlborough | $570 | $570 |

| Nelson/Tasman | Nelson/Tasman | $610 | $610 |

| Northland | Northland | $590 | $590 |

| Otago | Otago | $650 | $650 |

| Southland | Southland | $500 | $500 |

| Taranaki | Taranaki | $590 | $590 |

| Waikato | Waikato | $595 | $595 |

| Wellington | Wellington | $595 | $595 |

| West Coast | West Coast | NA | NA |

Most properties, more choice

Explore endless possibilities on NZ's favourite property app.

Download on iOS Download on Android

Author