Home loan and mortgage guides

Do your home loan homework

From working out what you can borrow to keeping an eye on the OCR, here's everything you need to choose a mortgage with confidence.

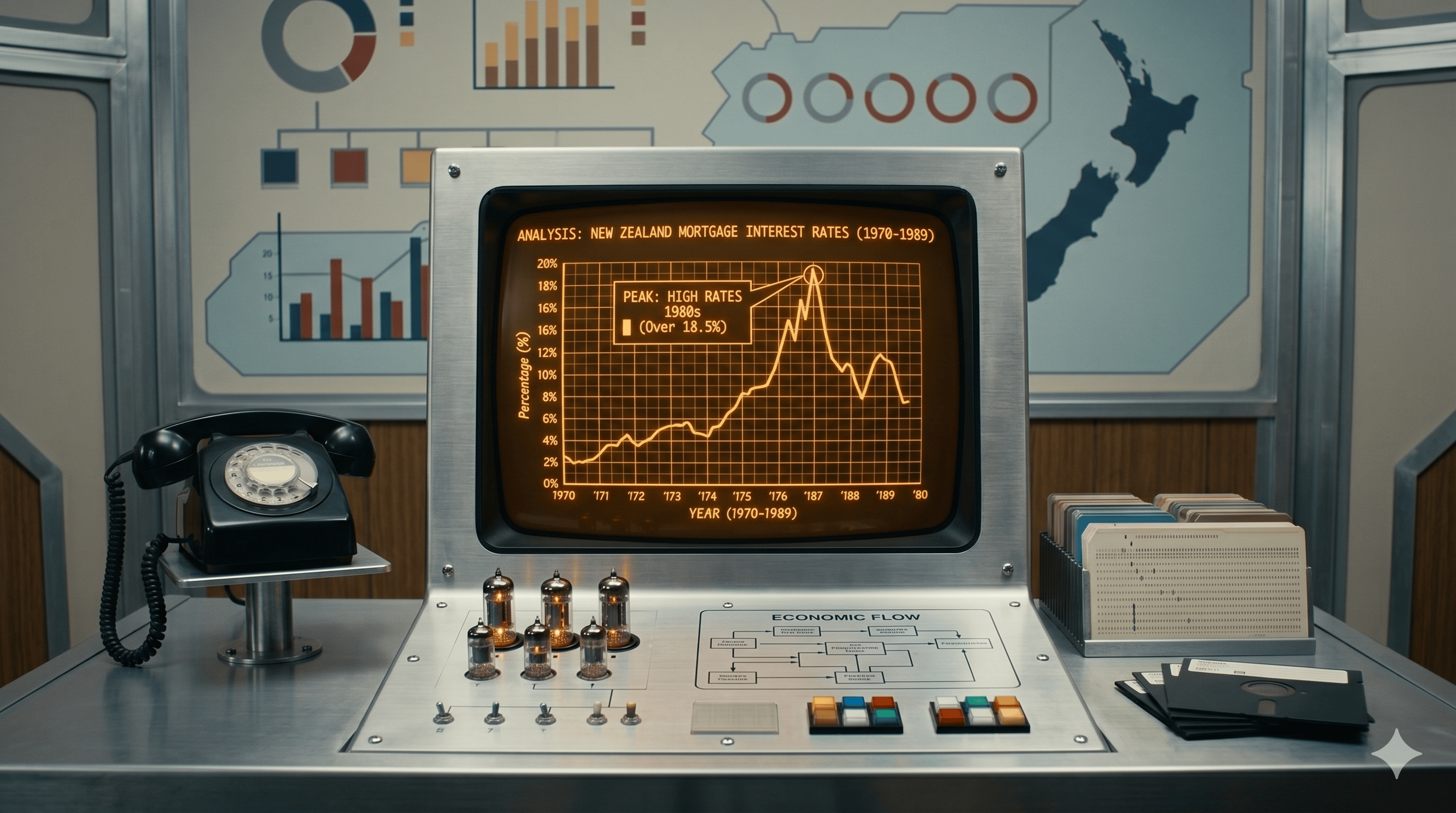

Interest rates and the OCR

Getting your first home loan

How much can I borrow?

Home loan guides

Latest News